In 1996, the Final Judgment in the Mojave River Basin Adjudication established a “physical solution” to address overdraft conditions and ensure that downstream users received sufficient surface or subsurface flow from upstream areas. The basin was divided into five hydrologically-related, but distinct subareas—Alto (Upper Basin), Baja (Lower Basin), Centro (Middle Basin), Este (East Basin), and Oeste (West Basin)—and water supplies within the subareas were apportioned among the producers.

A Base Annual Production (“BAP”) right was established for each producer in the basin. BAP is a producer’s maximum annual production from 1986 to 1990 and is used to determine the producer’s proportional share of the available water supply each year. BAP can be permanently transferred either independently or appurtenant to land.

In the first five years following entry of the judgment, the total BAP in each subarea was ramped down from 100% to 80%, and each year the watermaster evaluates conditions and determines if further ramp down is needed. The ramped down annual supply is allocated to the producers as Free Production Allowances (“FPA”). FPA specifies the amount of groundwater that a holder can pump without incurring a replenishment obligation. In 2016, FPA ranged from 45% of BAP to 80% of BAP, depending on the subarea. In the Alto subarea, it was set at 80% for agricultural users and 60% for municipal and industrial users.

Unused FPA can be carried over to the following year. Both FPA and carryover water can be transferred to another water user, who can use it to meet a replenishment obligation or to increase their allowed pumping for that year. While transfers of BAP, FPA and carryover water occur in all five subareas, the markets are the most robust in the Alto subarea, which includes most of Southern California’s high desert communities.

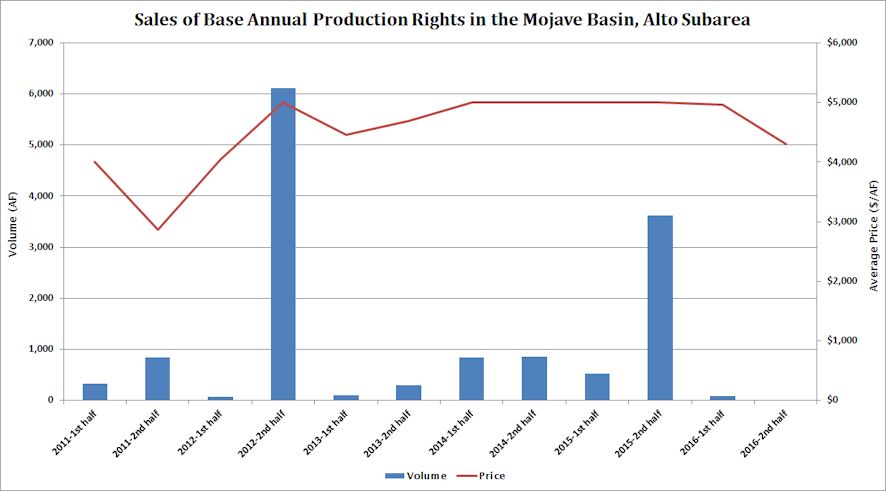

Sales of Base Annual Production Rights

Generally, the volume of Base Annual Production rights traded is small, with spikes in volume driven by the occasional large transaction. Activity was especially low in 2016, when 12 AF traded in the second half of the year, and 85 AF traded in the first half of the year. The second half of 2015 saw a total of 3,615 AF trade–with the spike in volume driven by a single large transaction—and the second half of 2014 saw 862 AF traded (see sales chart).

After generally trending upward since the inception of the market, prices have been sitting around $5,000/AF, but dropped to $4,300/AF in the second half of 2016.

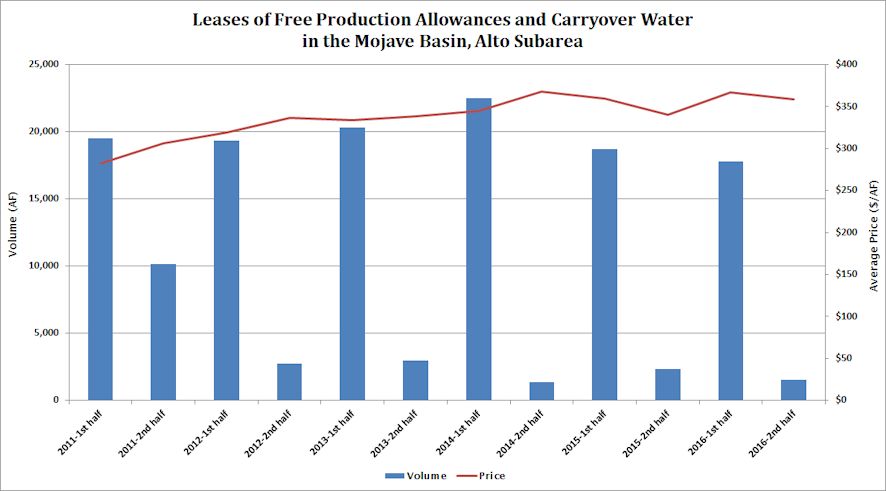

Leases of Free Production Allowances and Carryover

The volume of leases of FPA and carryover water in the Alto Subarea tends to fluctuate: high in the first half of the year and low in the second half. Because the Mojave Basin Watermaster operates on a fiscal year, the short-term transfers approved in the first half of the calendar year may reflect efforts to prepare for the new water year.

Leases totaled 1,506 AF in the second half of 2016—compared to 2,355 AF in the second half of 2015 and 1,332 AF in the second half of 2014. The first half of 2016 saw leases totaling 17,785 AF.

The average prices for leases of FPA trended upward from the inception of the market through the second half of 2014, when they reached a peak of $368/AF. Since then, they have been fluctuating near $360/AF. In the second half of 2016, prices were at $359/AF.

The market continues to be driven by the need for producers to meet their replenishment obligations, rather than any external pressures, so trends are likely to remain unchanged.

Written by Marta L. Weismann

You must be logged in to post a comment.