Demand for Lower Rio Grande water created a lease market in south Texas. Lease prices vary by use, with agricultural water users typically paying lower rates per acre-foot because they have lower consumptive use of water.

Municipal users have priority in the system, with a municipal reserve of 225,000 AF reestablished each month. Excess water is allocated to irrigators, who must have a balance available in a revolving account to take delivery of water. The long-term average allocation for Lower Rio Grande contracts is 2.5 AF/acre.

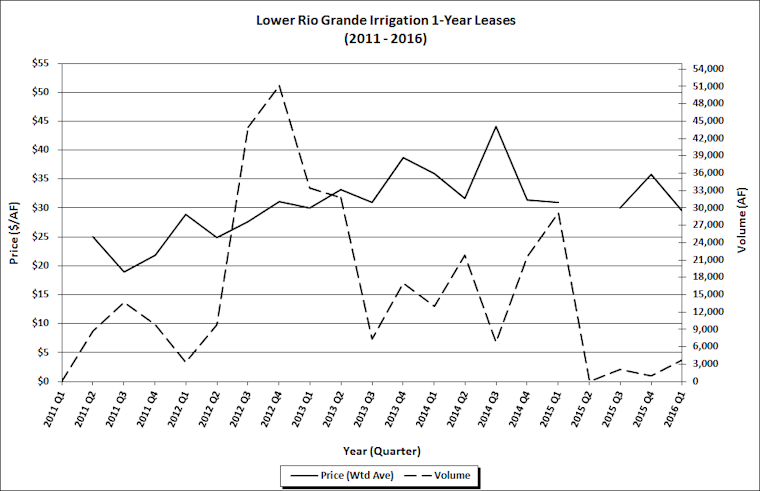

Between 2009 and early 2011, water supplies were abundant, so the watermaster was able to provide full allocations (4 AF/acre), and during flood operations at the Falcon and Amistad Dams, the Rio Grande Watermaster provided “free water” that does not count against contractors’ accounts. As a result, leasing activity for irrigation water was sparse during that time.

Heavy rain and flooding in the spring of 2015 led to a similar situation, depressing leasing activity for 2015. The low level activity has continued into 2016. During the 1st quarter of 2016, there were seven leases for irrigation water totaling 3,665 AF (with 2,500 AF accounted for by a single transfer from U.S. Fish & Wildlife to Delta Lake Irrigation District)—compared to 29,115 AF in the 1st quarter of 2015, no leases in the 2nd quarter, 2,045.20 AF in the 3rd quarter, and 987 AF in the 4th quarter (see chart).

Prices for irrigation water have eased. During the 1st quarter of 2016, prices ranged from $25/AF to $30/AF, with an average price of $29.42/AF—down from an average price of $35.78/AF in the 4th quarter of 2015. The average price was $30.91/AF in the 1st quarter of 2015 and $30/AF in the 3rd quarter of 2015. (There were no leases during the 2nd quarter of 2015).

Because municipal users have priority in the system, the market for leases of municipal water is usually thin. Activity for industrial use and mining is also limited. In the 1st quarter, there were no leases for municipal water. A total of 320 AF were leased for mining use at an average price of $400/AF.

When dry conditions resumed after the 2009-2011 wet period, so did leasing activity. The market peaked in the 4th quarter of 2012 with irrigation leases totaling 51,183 AF for just that quarter, and trading remained high—rivaling or exceeding the amount of activity seen during the drought of the late 1990’s.

If past behavior is the best indicator of future behavior, a similar pattern can be expected this time. However, a new question has emerged regarding whether Mexico’s recent repayment of its water debt under the Rio Grande Compact shores up supplies enough to impact market activity. (For more on Mexico repaying its Rio Grande Compact water debt, see “Mexico Retires Rio Grande Water Debt in Full,” JOW March 2016). Will higher leasing activity and higher prices return with drier hydrologic conditions?

Written by Marta L. Weismann

You must be logged in to post a comment.