Cadiz

Cadiz

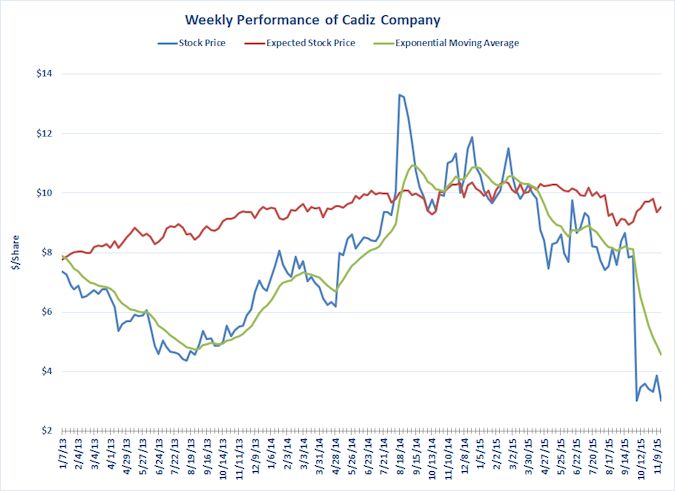

Cadiz (CDZI) stock price remains depressed since the release of a letter dated October 2, 2015 by the Bureau of Land Management determining that the Cadiz Project is not within the scope of the Arizona-California Railroad right-of-way over federal lands. If the determination stands, BLM believes that the Cadiz Project would need BLM approval for a right-of-way over federal lands for the project’s water conveyance pipeline. (For background the BLM determination, see “BLM Determines that Cadiz Project Needs Federal Approval,” JOW October 2015).

The price now stands 73.3% below the price 52 weeks ago (when its price fluctuated above $9/share) and 68.2% below its expected price. The stock price is only 66% of its 10-week exponential moving average.

CDZI price leaped in August 2014 with issuance of a court ruling dismissing all challenges to the project based on the alleged inadequacy of environmental review. The price had started declining in March 2014 when Business Week published a one-sided article about opposition to Cadiz’s Project.

CDZI stock had been underperforming relative to the returns forecasted by the Capital Asset Pricing Model by an annual rate of 6.1% from January 2006 through December 2012. The Company announced a comprehensive refinancing package in March 2013 to accommodate project financing for the Cadiz Valley Water Conservation, Storage and Recovery Project. The project faces litigation challenges, although the Company has been successful in securing dismissals or settlements in mid to late 2013. The company also secured further working capital from an agreement with a senior lender in October 2013. The turnaround in the company’s stock in the latter half of 2013 has closed the gap of stock performance relative to expected prices (projected by the Capital Asset Pricing Model adjusted by historical under performance).

Pico Holdings

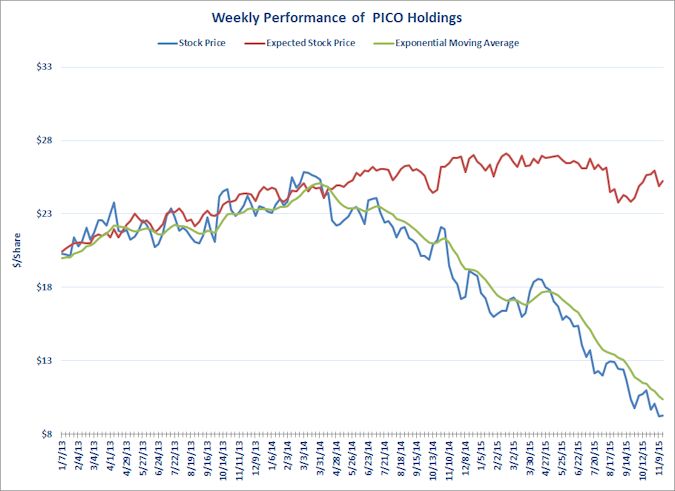

PICO Holdings (PICO) stock price remains in free fall. The price now stands 63.2% below its expected price. The company is suffering losses in its three major business segments: water resources and storage, agribusiness and real estate. PICO’s price has declined by 48.9% over the past 52 weeks. A recent price turnaround last April, which proved temporary, may have been prompted by the announcement that the firm has retained an investment banker to monetize its investment in Northstar (canola operations), one of the sources of operating losses. The price is 10% below the 10-week exponential moving average. When will PICO’s price reach bottom?

PICO stock had been underperforming relative to the returns forecasted by the Capital Asset Pricing Model by an annual rate of 4.9% from January 2006 through December 2012. The company’s stock has performed strongly in 2013, increasing by about 19% in 2013 in comparison to a decline in expected prices forecasted by the Capital Asset Pricing Model (adjusted by historical underperformance). Favorable developments for the company include a planned IPO for the company’s residential land development and residential homebuilding subsidiary, improvement in farming operations in production of canola oil and an option agreement to sell 7,240 AF of water rights in Lincoln County, Nevada to a power generation project at $12,000/AF.

You must be logged in to post a comment.